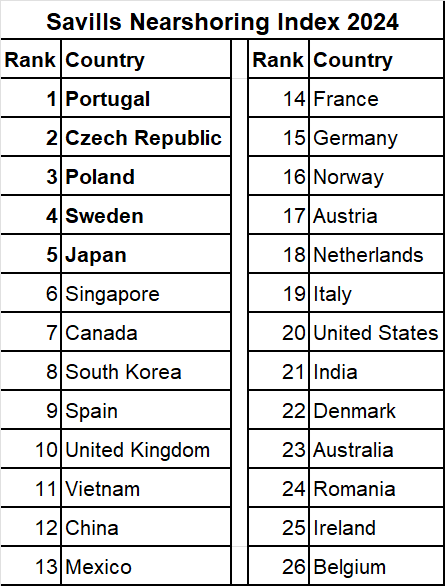

According to the 2024 Savills Nearshoring Index study, the Czech Republic is the second most attractive location for industrial occupiers looking to ‘nearshore’ supply chains. Portugal ranks first, Poland in third place, Sweden being fourth, and Japan rounding out the top five.

Savills 2024 Nearshoring Index ranks 26 countries on the factors that may be important to occupiers looking for new locations to shorten or diversify their supply chains and/or reduce their reliance on foreign imports. These factors include their resilience, economic cost (including rents, energy and labour costs), business environment and ESG performance. Savills says that depending on occupiers’ individual priorities, other locations further down the Index may be preferred, such as those where costs may be higher but have stronger environmental credentials and a better business environment, whilst others may perform exceptionally well but only in one pillar.

Savills 2024 Nearshoring Index ranks 26 countries on the factors that may be important to occupiers looking for new locations to shorten or diversify their supply chains and/or reduce their reliance on foreign imports. These factors include their resilience, economic cost (including rents, energy and labour costs), business environment and ESG performance. Savills says that depending on occupiers’ individual priorities, other locations further down the Index may be preferred, such as those where costs may be higher but have stronger environmental credentials and a better business environment, whilst others may perform exceptionally well but only in one pillar.

“Locations that score well in the Nearshoring Index’s economic cost pillar, however, don’t tend to score as highly for resilience, business environment and ESG. The exceptions are Poland, Portugal and the Czech Republic, which provide a rare combination of being low cost, resilient, and provide occupiers with access to the European single market,” says Ondřej Míček, Head of Industrial Agency at Savills Czech Republic.

Traditionally low cost hubs were the largest beneficiaries of the original wave of offshoring, as occupiers prioritised cost, but with the impacts of supply shocks and an increased focus on ESG performance, many are now weighing other factors in their decision-making process, although budgets are still a major driving force.

Charlotte Rushton, Analyst, Savills World Research says that when nearshoring began to emerge, there were concerns of a wholesale global supply chain upheaval. “What has occurred so far, however, is more subtle: manufacturing trends appear to show that although companies are setting up in new locations, they’re still prioritizing reducing costs, therefore favouring locations such as Mexico and Vietnam. But there are exceptions: some manufacturing, such as semiconductors, electric vehicles and energy, is more sensitive to geopolitics and trade policy, so occupiers here tend to prioritise higher-skilled and higher-valued production, and therefore favour locations such as Sweden, the UK and US.”

The problem with the term nearshoring of course, is that while recent shocks have definitely changed the way companies think about their supply chains, the trend is not nearly as obvious and clear-cut. So I asked Oliver Salmon, Director World Research at Savills, if it’s fair to say we’re still waiting for a visible wave of nearshoring investments.

Oliver Salmon: Yes, ultimately nearshoring will be driven by Government policy, subsidies and so on. Moreover many nearshoring requirements are driven by B2B factors rather than B2C factors, so are therefore more strategic in nature. We therefore expect nearshoring requirements to be more of a multi-year trend rather than the explosion of take-up we saw related to e-commerce, for example.“

ThePrime: My understanding is that while some companies may move some percentage of capacity closer to their consumer markets, the markets near their current production locations have become more attractive in their own right. In other words, rather than moving a whole factory back from China to Europe, a European company might be re-thinking whether to build another production facility closer to home markets.

Unravelling the existing complex network of global supply chains is difficult and expensive – there is a first mover disadvantage – so we’re seeing a slow and subtle change in location choice. There’s a couple of factors at play – occupiers want to be geographically close to their final consumers, but at a low cost also. On top of this, occupiers, having been scarred from Covid-related supply chain shocks, want a diversified supply chain to allow for continued smooth business operations even if there are disruptions in certain locations. So you’d be right to assume that occupiers aren’t necessarily closing all operations at factories in China (for example) but are looking at new and future facilities closer to key markets, as well as in other lower cost production centres. This is leading to strategies such as China+1 for example.

I’m surprised Northern Africa isn’t in the top 20…was all of EMEA considered?

We analysed 26 key manufacturing locations based, but the list the limited by data availability, specifically on warehousing costs. As such, no Northern African markets were considered for this analysis. We did analyse a larger set of markets (including a number of Northern African markets) in 2022, using a broader measure of cost, but none were in the top 20. As we included other indicators around the business operating environment and ESG, some Northern African countries benchmark less favourably on these metrics, as opposed to cost and proximity to large consumer markets.

I’m also surprised the US isn’t seen as more attractive. Cheap energy, huge market, potential tariff wars coming.

Those factors do help support the US market, but the US also has high costs in terms of rents and labour. From a more practical perspective, there is a lot of discussion of an American manufacturing resurgence, but this is largely concentrated in a few sectors that are more sensitive to geopolitics, as well as trade and industrial policy, such as semiconductors, dual-use technologies, energy, and energy-transition (e.g., EVs). As it’s part of USMCA, there’s been an increase in occupiers opening production facilities in Mexico aimed at suppling American consumers (including inbound Chinese investment).

In general, how is the potential for trade wars impacting investment decisions?

More than ever supply chain planners will be looking at global geopolitical issues in the context of their investment decisions. The potential for trade wars will be a factor in those decisions and if there is a degree of escalation that would suggest Europe would be a beneficiary for inward investment.

Flooded towns are just the latest victims of archaic planning system

Simon Johnson (Crestyl): Dornych will be a retail force in Brno