How did last year compare to 2022 in terms of Slovak investment transactions?

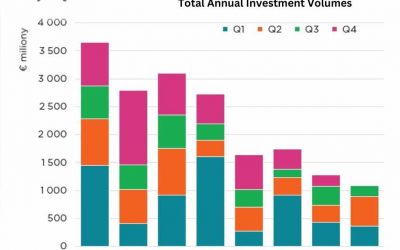

In 2023 we had investment volume of €664 million, which is a 41% decrease compared to 2022. 58% of the acquisitions were made by domestic investors, which is one of the highest in the region. In Poland, for example, they had just 7% of local investors. Here, 70% of all investments were for office building and 14% was into retail and industrial.

What caused the disappointing drop in volume?

The market was still affected by the war in Ukraine, by high inflation, high interest rates and energy costs. In fact, the average long-term investment volume is between €600 and €800 million, but in 2022, the liquidity was over €1.1 billion.

Of course, 2022 was a record year in a lot of countries. So, the poor y-o-y comparison for 2023 isn’t really so surprising.

If you compare it to other countries, Hungary was -67%, Poland was -65% and in the Czech volume was 16% lower. Overall, Europe was down by 47%, falling from €308 billion to €162 billion in 2023.

How do you see it this year?

How do you see it this year?

We expect a decrease in investment activity in general. We expect liquidity somewhere between 400 and 600 million. Liquidity will come mainly from the V4 countries and from Asia, meaning mostly logistics. But we expect a rental increase thanks to inflation as well as yield stability. We might reconsider these predictions if the ECB starts reducing interest rates, something we expect in June. Based on CBRE’s investment survey for the CEE region, more than 50% of all respondents believe the market will recover over the next 6 to 12 months. Looking at investment preferences in CEE compared to Europe, we see a clear correlation where demand for the office sector has dropped to 13% (CEE) and to 18% (Europe), but there’s a strong interest (one-third of European respondents) in the industrial and logistics sector. In CEE that figure is up to 44%.

Along with industrial, retail parks really came to the fore during the pandemic. Is that still a hot investment product?

We think retail parks are an underappreciated investment asset class compared to office buildings and shopping centers. They’re resistant to market fluctuations, as we saw during Covid, when they were the biggest winners. They have a stable vacancy rate (2-3% across Europe) and a stable rental mix. According to CBRE’s latest data, they show an increase of 9% rent increased in 2023 across Europe. One of the main advantages over shopping centers are the locations. They don’t have to be located in the city center, they’re usually located at the outskirts of cities or at busy traffic junctions. In recent years, we have recorded an increased in the number of completed retail parks in Slovakia: 19 completed ones with a total GLA of 94,000 sqm. They’re also very popular with investors, if you see that over the last five years over €100 million was invested in retail parks. For companies that own several retail parks, they seen an improvement in the negotiating position they have with tenants. Investors with a portfolio have more power to negotiate better terms and conditions in their lease contracts.

In Bratislava you probably have too many shopping centers. Will there be too many retail parks soon as well?

Retail parks are mostly developed in secondary and tertiary cities, so if you build one it’s unlikely there will be another one. Also, the development is driven by tenants. If you have a dm drogerie in one smaller city you won’t get another one. Tenants evaluate the situation and wouldn’t enter a neighboring project because they would hurt their turnover.

What are the yields?

Currently we are quoting a prime yield of 7.15% for retail parks, which is higher compared to logistics and office. Office is 6% and logistics 6.25%, so there is a big gap compared to the risk.

How do you explain the discount? It doesn’t make sense if there’s almost no vacancy and little competition.

It’s a good question. In part, it’s the current liquidity on the market. But basically, this why I say it has unappreciated investment potential which obviously can benefit an investor in the future with future value increase. The sharpest yield for retail parks in the past was 6.75%, and we expect that to return in the future.